The municipal bond market, long perceived as a safe haven for conservative investors, is currently teetering on the edge of a perilous transition. For decades, munis have maintained a reputation for stability, tax advantages, and reliable income streams. However, recent market indicators reveal a disturbing divergence: while other fixed-income assets continue their upward trajectory, munis are sinking into unprecedented territory of underperformance. This is not merely a cyclical blip but a profound structural shift that demands critical scrutiny. The entrenched assumptions about muni safety are no longer solid; instead, they are collapsing under the weight of multiple converging factors that threaten the very foundation of municipal finance.

What is particularly alarming is the stark deviation in market behavior. Year-to-date, long munis—those stretching beyond two decades—have plummeted approximately 4%. This collapse is disproportionate when contrasted with gains in corporate bonds, Treasuries, and bank loans. The typical safe harbor is evaporating, and skeptics are beginning to question whether the muni market has fundamentally lost its grip on stability or if this is a temporary blip driven by specific anomalies. The answer isn’t just academic—it spells trouble for investors, taxpayers, and policymakers alike.

Supply Overload and Evolving Investor Sentiment

One of the most glaring catalysts behind this disconcerting trend is the extraordinary surge in muni issuance. In the first half of 2024 alone, issuers flooded the market with approximately $280 billion worth of new debt. This overexposure, driven by fears related to potential legislation that threatened to eliminate tax-exempt status, caused many to rush issuance ahead of the purported tax law changes. The political landscape has since stabilized—the “One Big Beautiful Bill” was passed, preserving the tax exemption. Yet, the markets remain mired in oversupply, highlighting an essential truth: market performance isn’t just about policy, but also about the subtle and often unpredictable psychology of investors.

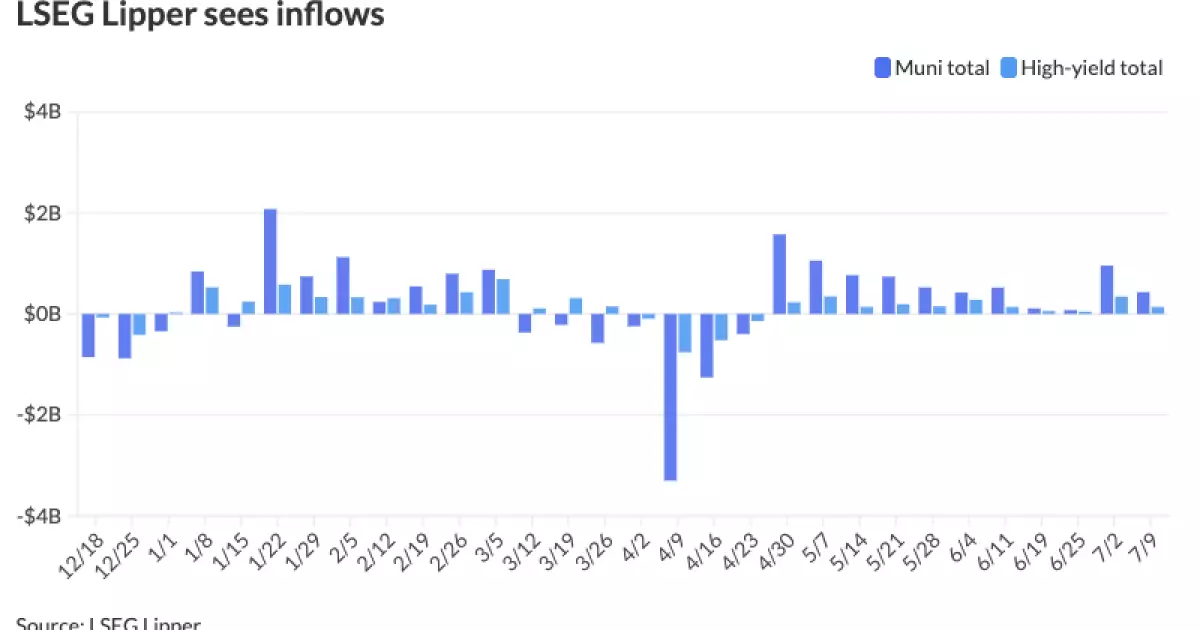

Investor behavior seems rooted in a complex mix of fear and herd mentality. Flows into municipal funds—both mutual and exchange-traded—have increased sharply, but not because of renewed confidence in the asset class. Instead, these inflows are more likely reactive, driven by a desire to anchor investments before the perceived savings diminish. Time and again, the market’s reluctance to extend past 15 years in duration signals an inherent caution or even aversion among large institutional investors. They are signaling that ries in the long end of the curve might be structurally unappealing, reflecting a collective skepticism about muni bonds’ resilience.

Economics, Policy, and the Future of the muni market

Adding another layer of complication is the intersection of macroeconomic policy and municipal finances. The Federal Reserve’s potential rate cuts in the fourth quarter of 2024 could ignite a risk-off rally that briefly benefits municipal bonds. But this is a double-edged sword. An environment of falling interest rates might temporarily buoy the market, but it also risks exacerbating underlying issues: budget constraints, inflated costs of infrastructure projects due to persistent inflation, and the waning of pandemic-era aid programs.

Furthermore, the breakdown in the traditional relationships—like the muni-UST ratio—suggests a deep-seated malaise. The yield curves are steepening in ways that defy conventional wisdom, hinting at investors’ growing unease with long-term municipal debt. This steepening isn’t merely a technical anomaly; it reflects an established preference for shorter-term holdings, hinting at a systemic reassessment of muni risk-premiums. The fact that munis are experiencing year-to-date losses while other assets thrive undermines the narrative of munis as a perpetual safe haven.

The variability of supply, investor flow dynamics, and macroeconomic shifts pose an urgent question: are these just external shocks, or are we witnessing an irreversible transformation? The market narrative often leans toward cyclical explanations, but the evidence suggests the challenge might be more structural, requiring a redefinition of what “safety” means in municipal investing.

Strategic Implications and the Path Forward

For investors committed to the municipal space, these developments demand a more nuanced and skeptical approach. Rational allocation now requires scrutinizing the underlying fundamentals of individual issuers, considering shifting supply-demand balances, and recognizing that traditional duration strategies may no longer be sufficient. The industry’s historical reliance on stable tax-exemption and longstanding infrastructure needs is being overshadowed by immediate liquidity concerns and risk reassessment.

Policymakers and market participants must also question whether the current dislocation exposes a deeper flaw—a disconnect between perceived safety and actual risk, especially in sectors reliant on municipal revenues and governmental backing. The potential for structural change, whether adapting to new political realities, fiscal constraints, or investor preferences, cannot be ignored.

The looming possibility that the muni market could remain in a distressed state for years challenges the long-held belief that municipal bonds are the ultimate safety net. Instead, a prudent strategy involves a critical review of asset allocation, a focus on quality over quantity, and an acknowledgment that the world’s perception of safety in munis is shifting—perhaps permanently.