Municipal bonds—long celebrated as a bastion of safety for conservative investors—have recently projected a veneer of calm and resilience that might be dangerously misleading. While muni yields experienced slight upticks early in the week and Treasury yields declined modestly, the broader picture reveals a marketplace resting on tenuous technical conditions rather than robust fundamentals. The muted volatility that pervaded June and crept into July provides a false sense of security. Dealers’ enthusiasm for any attractively priced deals only paints half the picture; behind that demand hides an unsettling lack of genuine catalysts to ignite sustained muni outperformance.

This shaky undercurrent exposes how reliant the municipal bond market remains on external forces—particularly fund flows and reinvestment patterns. Indeed, while municipal mutual funds have enjoyed nine consecutive weeks of inflows, these inflows remain modest in scale relative to what would be needed to fuel a true rally. The market’s cautious reception to generous spread levels indicates a crisis of confidence: investors know munis are “cheap” but can’t justify pushing prices significantly higher without clearer triggers.

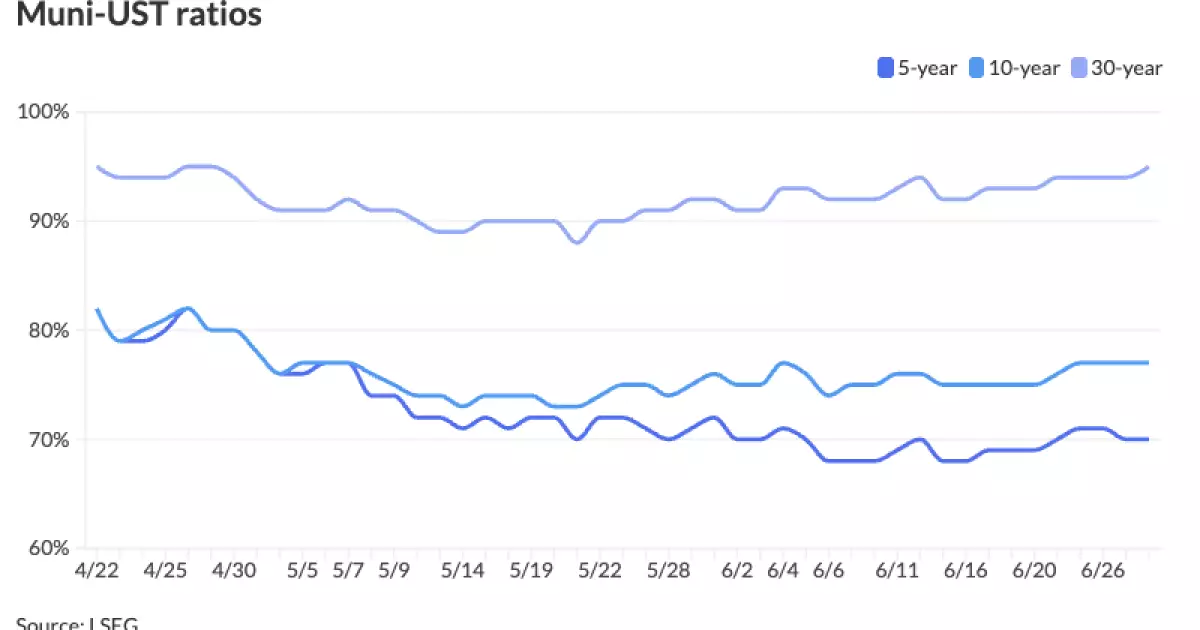

Distorted Yield Ratios: Are Municipals Overvalued or an Opportunity Waiting to Happen?

Closer scrutiny of muni-to-Treasury yield ratios reveals intriguing, yet alarming, dynamics. Shorter-duration munis are yielding roughly two-thirds of their Treasury counterparts, with ratios hovering between 66% and 70% in the 2- to 5-year maturities; longer maturities are nearing parity. On surface, ratios under 100% might signal value, but in reality, they often reflect shifting risk appetites and tax-equivalent yield calculations that can mislead less savvy investors.

The tax-sheltered nature of municipal debt inflates comparative attractiveness, yet the premium paid for this exemption has compressed dangerously during times of increased credit and liquidity risk. As after-tax spreads drift wider, especially on long-end bonds, the market signals caution rather than eagerness. Even high-grade (HG) deals boasting after-tax yields above 8% should not be blindly embraced without factoring in evolving economic headwinds and municipal credit challenges.

The Reinvestment Cliff: A Double-Edged Sword Threatening Market Balance

Arguably the most underappreciated factor lurking beneath recent muni market movements is the massive July reinvestment outflow. Investors are poised to receive around $40 billion in principal repayments plus an additional $14 billion in interest for the month—a nearly 50% jump from the yearly average. This flood of cash creates a critical juncture: the market must absorb a tidal wave of incoming liquidity, or risk unsettling price disruptions.

Dominant redemptions come from fiscal heavyweights like California, New York, and Florida—states facing their own budgetary pressures amid shifting federal support dynamics. The new-issue calendar is relatively sparse during the Independence Day week, constraining opportunities to reinvest that vast principal and interest. When new issuance fails to keep pace with available liquidity, the delicate balance between supply and demand can fracture, producing volatility masked by currently subdued headline movements.

Primary Market Strength: Not a Panacea for Municipal Fixed Income Woes

In sharp contrast to secondary market lethargy, the primary municipal market continues to gather steam with considerable investor appetite. Recent deals have priced with wide spreads, attracting heavy subscriptions—a testament to persistent demand for yield in a world starved for income. However, this strength is misleadingly concentrated. The apparent “star of the show” status of primary issuance belies the absence of genuine long-term conviction.

Even blockbuster deals scheduled later this month—including large bond offerings from California’s Community Choice Financing Authority, New York’s State Thruway Authority, and the New York City Transitional Finance Authority—face an uphill battle to maintain favorable pricing environments. Subdued macroeconomic signals and the specter of rising rates amplify underwriting risks, and investors’ willingness to embrace these deals hinges precariously on tax benefits rather than unshakeable credit confidence.

Political Uncertainty and Fiscal Challenges: The Imperfect Shield of Tax Exemption

The municipal bond market’s oft-touted tax advantage acts as a profound lure, but it does not inoculate against fiscal mismanagement or shifting political winds. Recent periods of low volatility belie significant pressures simmering beneath the surface—state and local governments grapple with budget shortfalls, pension obligations, and pandemic recovery costs. Compounding these structural challenges is the unpredictable nature of federal policy, which can shift credit support or interest deductibility overnight.

From a center-right liberal standpoint, advocating fiscal discipline and transparent governance is fundamental to restoring genuine confidence in munis. The reliance on generous after-tax yields to attract investment disguises deeper fragilities and promotes complacency toward municipal fiscal reform. Investors should demand that munis mirror the accountability embedded in private sector debt, rather than resting on political goodwill or tax shelters.

The Treasury Bond Shadow: Munis’ Dependence on Broader Market Trends

Municipal yields do not operate in isolation; their movements are closely tethered to Treasury benchmarks. Recent downward moves in Treasury yields—particularly in the medium-to-long term—have buoyed muni valuations. However, this tether is a double-edged sword: rising rates spurred by inflationary concerns or Federal Reserve tightening could swiftly undercut muni demand, squeezing yields higher and prices lower.

The two- to five-year Treasury yields edging down by several basis points paradoxically highlight how vulnerable munis are to macroeconomic inflections. Without independent momentum, the municipal market’s fate remains entangled with federal monetary policies over which state and local issuers have no influence. This dependency underscores the risk of complacency among muni investors expecting a “safe haven” insulated from broader market gyrations.

Missing the Catalyst: Why the Muni Market Might Face Headwinds Ahead

Ultimately, the most glaring weakness in the municipal bond landscape is the glaring absence of a market catalyst. Investors are caught between recognizing the sector’s cheapness and lacking a compelling reason to accelerate exposure. Without significantly higher fund inflows or a sudden credit upgrade environment—and with a reinvestment wave threatening liquidity imbalances—the municipal bond market appears vulnerable to stagnation or episodic declines.

This dynamic is a cautionary tale for conservative portfolio managers and retail investors alike: perceived safety in munis is context-dependent and fleeting if structural fiscal or macroeconomic shocks emerge. Taking a passive stance simply because munis carry tax benefits disregards underlying risks and political nuances. More prudent is a selective approach rooted in credit analysis and timing, rather than blind acceptance of muni bonds as inherently low-risk instruments.