The municipal bond market has recently demonstrated a steady state with little statistical change, even amidst a backdrop of fluctuating U.S. Treasury yields. Investors have predominantly opted for tax-exempt municipal bonds, bolstered by substantial inflows into mutual funds. As reported on a Thursday, with U.S. Treasury yields inching upward and equity markets closing in the red, the municipal ratios remained relatively stable, signaling a point of resilience within the sector. According to multiple sources, including Municipal Market Data and ICE Data Services, ratios have shown minimal shifts, indicating investor confidence and demand primarily focused on longer-dated securities.

The municipal sector appears somewhat insulated from the recent uptick in Treasury yields—a trend reflected in the comments from industry experts. Kim Olsan, a senior fixed-income portfolio manager, noted that while long-term UST yields were experiencing upward pressure, the municipal market’s pricing dynamics remained unaffected. In particular, the 10-year and 30-year municipal offerings have not surged in response to a similar rally seen in UST yields, suggesting a disconnect in market perceptions between taxable and tax-exempt securities.

This perceived stability may be a reactionary safeguard against volatility, particularly as a combination of steady inflows and stable demand allows investors to perceive value beyond surface-level yield fluctuations. Moreover, strong follow-through on transactions indicates a robustness for tax-exempt trading, though long-term bonds still seek to attract additional performance amidst this competitive space.

The significance of maturities stretching beyond 12 years cannot be overstated; current data indicates these long-term bonds have come to comprise 55% of total tax-exempt trading volume, marking an increase of approximately 5% to 7% in recent weeks. This trend underscores a preference for high-quality municipal issues, often featuring competitive yield pickups. With states like Ohio offering 5% coupons sharply contrasted against lower yield benchmarks, the market continues to pivot towards favorable long-end opportunities for investors seeking greater returns in a climate of relatively negative supply.

High-quality general obligation bonds, particularly those with solid backing and robust demand, are becoming increasingly attractive. Olsan’s observations highlight that bonds with extended maturities can yield compelling rates, suggesting that investors remain strategically positioned to exploit such disparities.

Transitioning to the primary market, this robust interest in long maturities has triggered a series of upsized bond offerings from issuers. Notably, the upsizing of notable issues like the South Carolina Public Service Authority’s and New York City’s financing initiatives reflects increased issuer confidence and investor appetite in long-dated securities. The significant adjustments in these offerings signal an acknowledgment of heightened demand and an anticipatory posture towards favorable pricing mechanisms.

Such adjustments illustrate proactive measures by municipal entities to capitalize on favorable market conditions, avoiding suboptimal supply limitations. The newly established yield curves created by these adjustments imply that while some states may experience an oversaturation of supply, others remain dramatically undersupplied, amplifying overall interest in high-quality offerings.

Disparities extend across different regional markets, with states like New York and New Jersey wrestling with significant negative supply figures. New York, for example, faces a daunting net balance of approximately $2.21 billion, alongside an additional $1.06 billion deficit in New Jersey. These scenarios create further competition within state-specific municipal sales, adding layers of complexity to investor and issuer strategy.

Conversely, areas such as Texas are experiencing conditions likely to encourage tightening credit spreads, particularly pertaining to school districts benefiting from strong ratings through support mechanisms. As such discrepancies fluctuate, the nature of local demand, regional credit ratings, and prospective financial trajectories will increasingly dictate bond performance.

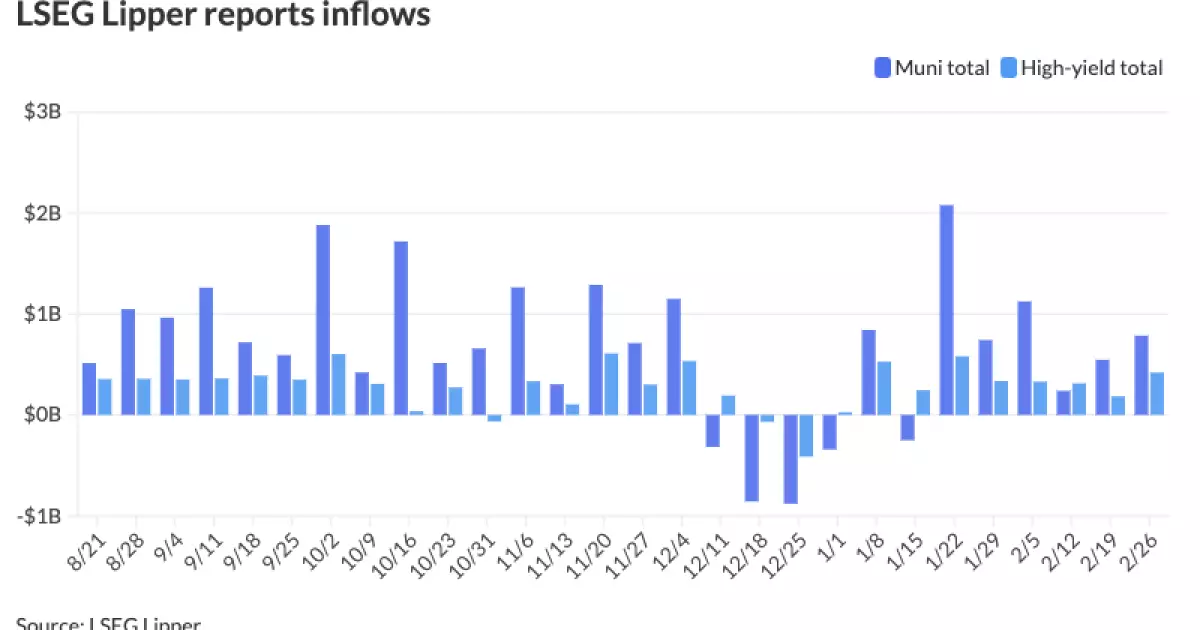

Reflecting on current inflow trends, recent weeks have seen significant additions to municipal bond mutual funds, suggesting that there exists an underlying confidence permeating among investors. With high-yield funds particularly gaining traction, as highlighted by strong inflows, the momentum perhaps points to an increasing attraction towards municipalities amidst broader market uncertainties.

As we approach the forthcoming issuance and redemption cycles, experts anticipate opportunities that could arise against a backdrop of measured volatility. The nuanced interactions of negative supply, regional disadvantage, and heightened demand could offer valuable prospects for investors while posing challenges to municipal issuers navigating an evolving economic landscape.

The municipal bond landscape demonstrates notable resilience amidst fluctuating yields and investor dynamics. The interplay of demand, regional discrepancies, and emergent opportunities will shape the fabric of the market moving forward, warranting careful scrutiny and strategic planning for investors and issuers alike.