The municipal bond market is often hailed as a bastion of stability for conservative investors, boasting tax-exempt yields and traditionally steady returns. However, a deeper dive into recent data reveals a less comforting truth: the muni market is grappling with substantial headwinds, posing a risk that many complacent investors overlook in the current climate of record issuance and shifting interest rates. Far from being an unshakeable safe haven, municipal bonds today stand precariously at the crossroads of oversupply, rising Treasury yields, and fragile investor sentiment.

The Illusion of Steadiness Amidst Record Supply

June 2025 marked a milestone in municipal bond issuance, with supply hitting an eye-watering $50 billion—the highest monthly total for this year and among the largest historically. This flood of new supply is no minor blip; it’s reshaping the landscape. The market’s reaction has been telling: tax-exempt bonds have noticeably underperformed Treasury securities throughout the month, with muni-to-Treasury ratios widening significantly, especially in the longer maturities. This divergence signals that municipal bonds, despite their tax advantages, are losing their premium status as demand struggles to keep pace.

Such an unprecedented surge in issuance is fueling concerns. Some major financial institutions, including BofA Securities, have revised their annual muni issuance forecasts upward to $580 billion from $520 billion, underscoring the market’s relentless expansion. Yet this growth is risky. It risks saturating the market, depressing prices, and squeezing yields upward to the detriment of existing bondholders. The picture is clear: investors are facing a supply glut at a time when compete attractiveness in other fixed income sectors—in particular Treasuries—has intensified.

Borrowers Win, Investors Lose: The Supply/Demand Mismatch

One of the key dynamics invalidating the prevailing bullish narrative is the disequilibrium between new issuances and redemptions. While the first half of 2025 saw record issuance ($275bn), projections for the second half paint a mixed picture. BofA strategists anticipate $308 billion in new issuance, but crucially, this is tempered by $337 billion in principal redemptions and coupon payments, theoretically alleviating pressure.

However, Barclays predicts a different trajectory, forecasting a 10% decline in second-half issuance yet cautioning that the muni market’s traditional summer strength in July and August—often driven by robust technical conditions—is fragile. Historically, muni-to-Treasury ratios decline modestly during these months. But given the current supply glut, even these seasonal tailwinds might be insufficient to bolster valuations significantly. Effectively, bond issuers stand to benefit from easy access to capital, but investors must grapple with an environment where oversupply chips away at returns and increases volatility.

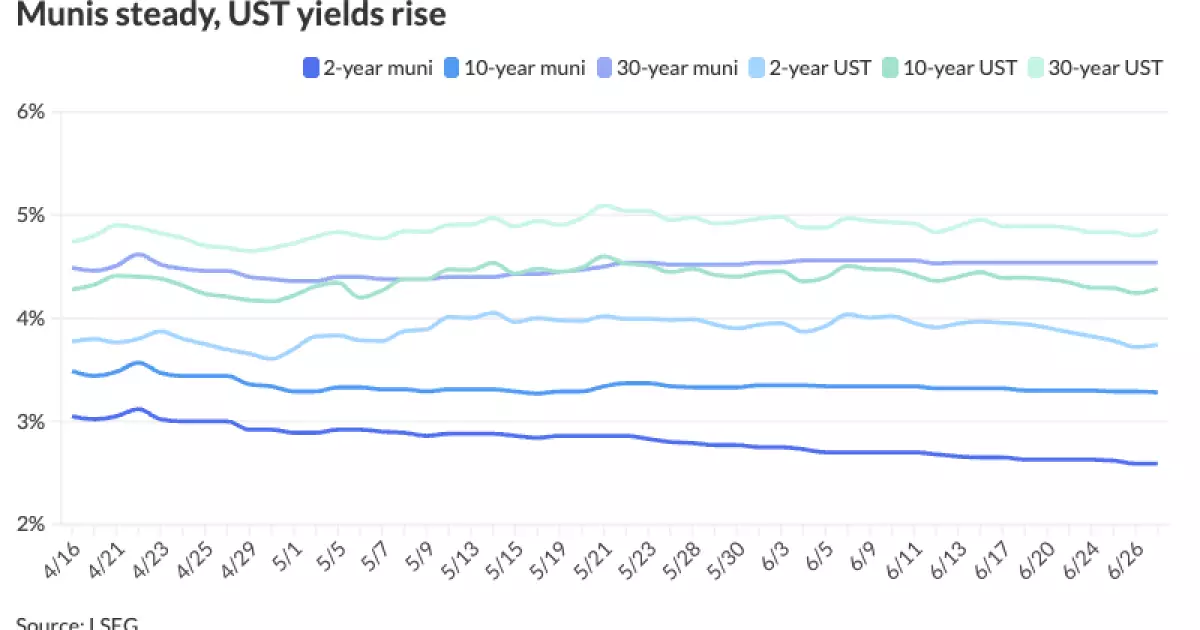

Rising Treasury Yields: The Silent Threat

Municipal bond yields do not operate in a vacuum, and current market conditions illustrate the interconnectedness with Treasury rates more than ever. Treasury yields have climbed steadily—2-year notes approached 3.75%, and 30-year bonds flirted with 4.85%. This rise creates a dual challenge. First, it pushes up the cost of borrowing for future municipal debt. Secondly, and more crucially, it increases the opportunity cost for investors in existing muni bonds, eroding prices and narrowing the relative appeal of tax-exempt debt.

Interestingly, despite the rise in Treasury yields, municipal bonds have not kept pace. Ratios of muni yields to Treasury yields — an important gauge of relative value — have moved upward, indicating muni bonds must offer higher yields to attract buyers. This shift exposes the muni market’s sensitivity to broader interest rate trends, undermining its perception as a decoupled asset class insulated from federal borrowing dynamics.

Why Investors Should Resist the Allure of Tax-Exempt Complacency

The political rhetoric extolling municipal bonds often touts their tax advantages and safety, anchoring them as core holdings for risk-averse portfolios. Yet, the current market environment demands prudence. The underperformance of munis year-to-date—remaining the only fixed income segment in the red—raises red flags for any investor blinded by conventional wisdom.

From a center-right, economically liberal viewpoint, the surge in issuance can be partially attributed to profligate state and local government borrowing, enabled by low borrowing costs during previous years and now increasingly costly as Treasury yields rise. Government entities are incentivized to issue new debt despite warning signs that investor appetite is waning, a dynamic that portends trouble down the road as the cost of servicing debt increases.

Investors should resist the temptation to overweight municipalities purely for their tax-status, especially when supply is at record highs and valuations suggest a price correction could be imminent. Instead, cautious investors would be wise to scrutinize individual credits more stringently and temper their expectations for muni returns in the near term. The market is not immune to macroeconomic shifts, and complacency could be costly.

Looking Ahead: A Back-Loaded Recovery, or a Slow Burn?

Optimists argue that the muni market’s pain is temporary and performance will be back-loaded, with better returns expected in the latter half of 2025 as issuance potentially declines and redemptions rise. While this may hold some truth, the fundamentals caution against overenthusiasm. The sheer magnitude of supply inflating the market in the first half is not easily reversed, and external risks—from inflation pressures to changing fiscal policies—could derail even the most optimistic scenarios.

More importantly, the behavioral aspect cannot be ignored. Investor psychology, shaped by persistent negative returns and widening muni-to-Treasury spreads, may lead to continued outflows or a wait-and-see stance, which prolongs the period of weakness. The “safe” mantle of munis now requires diligent risk assessment rather than blind faith in tax exemption benefits.

In short, the municipal bond market is at a critical juncture. It requires a recalibration of investor expectations and a recognition that, despite superficial steadiness, underlying market forces threaten the narrative of muni resilience. For those guided by center-right economic sensibilities, questoins about fiscal responsibility, borrowing sustainability, and market discipline must take center stage in portfolio decision-making.