As the Federal Reserve approaches its anticipated meeting on December 18, speculation abounds concerning a potential interest rate cut of 25 basis points. This would represent the third consecutive reduction, amounting to a total decrease of one full percentage point since the Fed began adjusting its policy in response to the highest inflation rates seen in four decades. Such actions underscore the central bank’s continued recalibration of its monetary policy to stabilize the economy, balancing the pressures of inflation with the necessity of fostering growth.

Jacob Channel, a senior economic analyst, hints at a cautious optimism amid uncertainty surrounding future fiscal policies under President-elect Donald Trump. The Fed’s decision-making process suggests a tendency to adopt a “wait-and-see” strategy, which may indicate an impending pause in rate cuts following December’s anticipated move. The various implications of high interest rates have rippled through many facets of consumer borrowing, impacting everything from credit card debt to auto loans and mortgages.

The federal funds rate—a crucial benchmark in the financial system—is essentially the interest charged between banks for overnight loans. While it doesn’t directly dictate consumer rates, changes in this rate influence what consumers ultimately pay for loans and receive on their savings. A cut could lower the overnight rate to a range between 4.25% and 4.50%, potentially easing some financial strain on consumers, yet experts caution that this shift may not provide comprehensive relief.

It’s critical to understand how these interest rate changes interact with various types of debt. Credit cards, which typically utilize variable rates, are particularly sensitive to shifts in the federal rate. Following the aggressive rate hikes observed from March 2022 to the current period, the average credit card interest rate has surged from 16.34% to an alarming 20.25%. Despite the Fed’s September initiation of rate cuts, consumers have yet to see a significant downturn in these rates. Greg McBride from Bankrate notes that lenders tend to act slowly when decreasing rates, creating a lag of up to three months. Given that many consumers possess substantial credit card debt, switching to 0% balance transfer offers may be more beneficial than waiting for a rate decrease that might not substantially ease their burden.

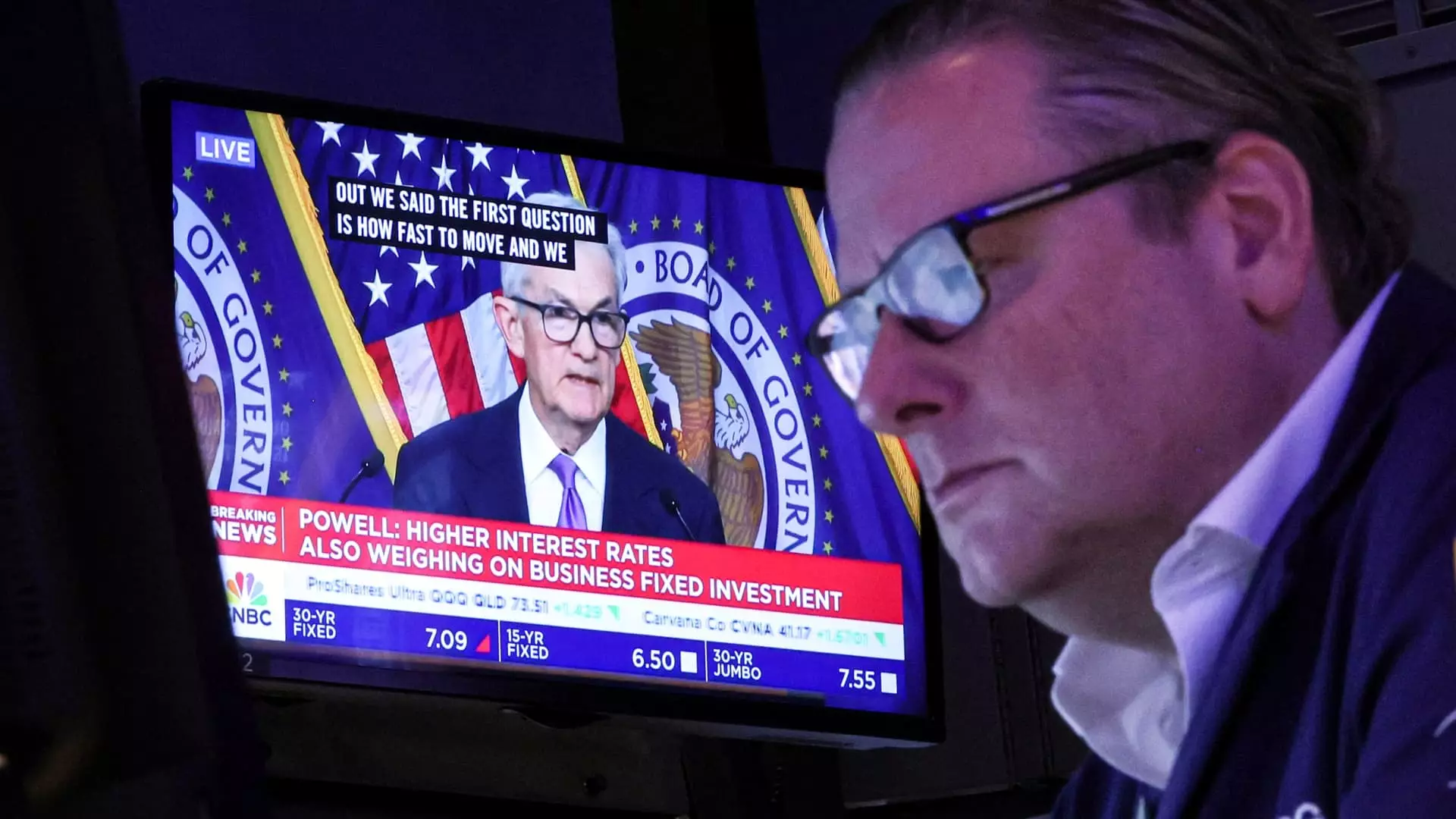

Fixed-rate mortgages, in contrast, operate under a different paradigm. Since most homeowners have locked in their mortgage rates, changes in the federal funds rate will not alter existing mortgages unless homeowners decide to refinance or sell their properties. As of early December, the average 30-year fixed-rate mortgage sits at about 6.67%, slightly reduced from the previous month but still substantially above the low seen in September. Economic analysts like Channel indicate that fluctuations in mortgage rates could persist, driven by variables beyond the Fed’s immediate influence, thereby complicating forecasts for prospective buyers.

Auto loans represent another area where consumers feel the weight of increasing interest rates. Although these loans are also fixed, consumers are dealing with rising sticker prices and, consequently, higher monthly payments. Drawing attention to the financial strain, the average new car loan rate around 7.59% is exacerbated by the noticeable increases in car prices. While potential cuts could theoretically offer relief, McBride emphasizes that high loan amounts—averaging around $40,000—play a more significant role in monthly budgeting challenges than rate cuts alone.

The situation with student loans reveals another layer of complexity. While federal student loan rates remain fixed, private loans can vary depending on their terms and are sometimes tied to Treasury yields. As the Fed continues to cut rates, borrowers with variable-rate private loans may witness a decrease in their payments. Mark Kantrowitz, a higher education expert, notes the importance of careful consideration when refinancing federal loans into private options, stressing the forfeiture of essential safety nets that federal loans provide.

Lastly, while the Fed’s adjustments do not have a direct impact on deposit rates, the correlation between the federal funds rate and savings account yields means that higher rates have historically benefited savers. With top online savings accounts still offering near 5% returns, McBride reassures that this remains a favorable time for those looking to save.

The Federal Reserve’s expected interest rate cuts may provide a mix of relief and continued challenges for consumers. As borrowers navigate the intricacies of credit cards, mortgages, auto loans, and student loans, understanding these changes will be crucial in making informed financial choices. Whether consumers can fully benefit from future rate cuts remains to be seen, and caution will be essential as they adapt to a fluctuating economic environment.