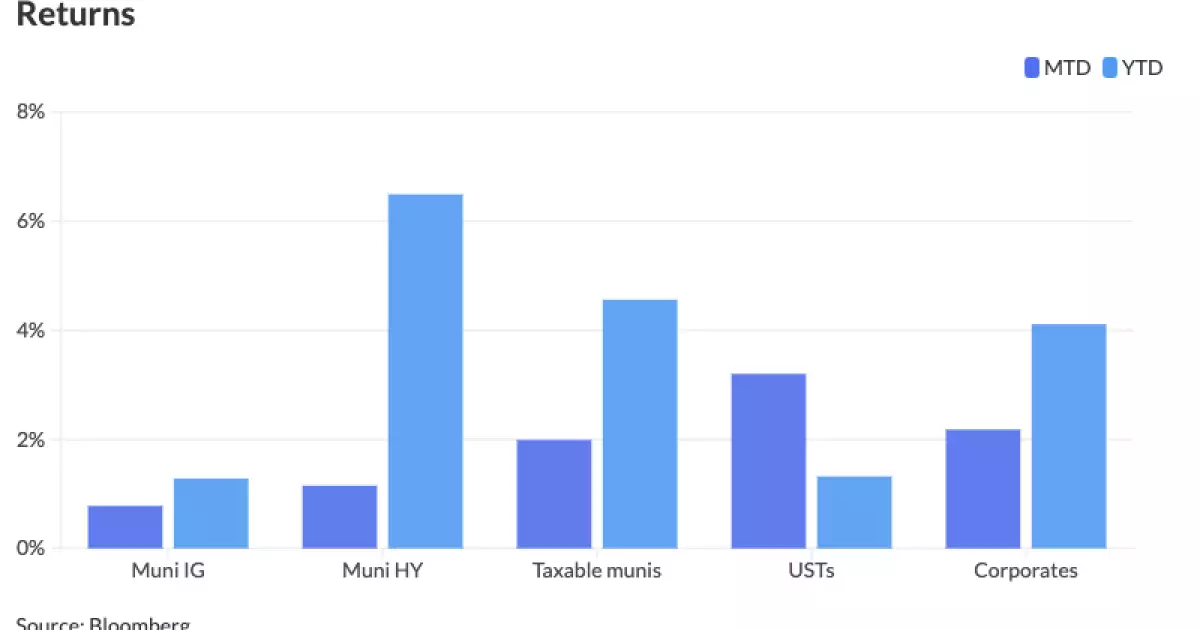

On Monday, municipal bond markets exhibited relative stability amidst a backdrop of slightly softer U.S. Treasury yields and a mixed performance in equity markets. This situation suggests a cautious sentiment among investors as they navigate the complexities of current economic indicators and Federal Reserve policies. Municipal bonds have historically been viewed as a safe haven, and their resilience this month, showing a gain of 0.78% so far, signals a unique market trend as we approach the end of August.

Comparative Yield Analysis

Reflecting on yield ratios, the relationship between municipal bonds and their Treasury counterparts has remained favorable. For instance, as of Monday, the two-year ratio registered at 62%, while the 30-year reached as high as 87%. This trend indicates a strong demand for long-term municipal bonds, which might be perceived as less risky amid economic uncertainty.

Data from ICE Data Services corroborates these findings. The two-year municipal bonds are yielding 43%, with similar patterns noticeable in the three- to ten-year categories. The yields across the board have been oscillating due to ongoing dialogues regarding Federal Reserve rate adjustments, which have dramatically shifted market expectations.

Jason Wong, vice president of municipals at AmeriVet Securities, pointed out that municipal bonds have generated a year-to-date total return of 1.28%. This is a stark contrast to the previous year when August ended with a decrease of 1.79%; a reflection of aggressive rate hikes instituted by the Fed to tackle rampant inflation. Observably, August 2023 has brought with it an average yield increase across the curve of approximately 26 basis points, particularly affecting the 10-year notes which escalated by 36 basis points within the month.

However, despite these increases, Wong noted that yields for 10-year municipal bonds have seen a slight reprieve recently, decreasing by an average of 2.5 basis points month-to-date. This drop aligns with speculation that the Federal Reserve may soon pivot to a more dovish stance influenced by Powell’s recent statements, potentially steering municipal yields lower.

The recent performance of the municipal market indicates a summer slowdown, attributed to seasonal holidays and traditional market inactivity. Chris Brigati, a senior vice president and director of fixed-income research at SWBC, emphasized that investor focus has shifted towards new bond issues over the last week amidst changing market conditions. A noted trend is that while the market has been less responsive to U.S. Treasury volatility, there have been signs of rising interest, particularly in the longer durations, where 30-year municipal-to-Treasury ratios approached 90%.

In a recent weekly report, Birch Creek strategists mentioned that a surge in separately managed accounts provided a boost to the short end of the MMD yield curve by approximately 12 to 13 basis points. Additionally, upcoming issuance is expected to remain above average, although cash reinvestment conditions may decline as we approach the Labor Day holiday.

Upcoming Issuance and Market Expectations

Looking ahead, this week’s average anticipated issuance of $8.9 billion marks a balanced approach to meeting investor demand while also navigating seasonal effects. Major upcoming issuances include a substantial $1.1 billion from the North Texas Tollway Authority and $1.8 billion from the New York City Transitional Finance Authority. This trajectory hints at continued municipal engagement, even as next week’s supply may ease due to the holiday.

As for yields, the Refinitiv MMD scale shows stability in AAA-rated municipal bond yields, suggesting little change in sentiment. Despite the slight adjustments noted in various yield curves—including the ICE AAA yield curve—the overall environment remains relatively stable for investors looking for safe, long-term investments amid fluctuating Treasury rates.

As the municipal bond sector continues to navigate this evolving landscape shaped by Federal Reserve policies and macroeconomic conditions, investors must stay keenly aware of market movements and interest rates. The resilience observed in municipal yields and pricing relative to U.S. Treasuries will be critical as we transition into September. With issuances on the horizon and the potential for policy shifts, strategizing investments within the municipal bond market remains essential for optimizing returns in this complex environment. The current state of the market not only underscores the inherent qualities of municipal bonds as a reliable investment but also invites scrutiny over their future performance as economic dynamics shift.