The municipal (muni) bond market has recently undergone a notable transformation, which has invited attention from investors seeking stability amid economic unpredictability. As we delve into the dynamics of this sector, it’s vital to explore the various factors influencing securities, yields, and overall market sentiment.

On the surface, the municipal bond market has shown a steady performance as of late January. As per Jason Wong from AmeriVet Securities, munis are enjoying a 0.43% gain for the month, pushing their year-to-date performance to 0.94%. This is particularly remarkable considering the disheartening -1.46% performance seen in December. Daryl Clements of AllianceBernstein reflects on this recovery, emphasizing that recent rallies have effectively overshadowed previous losses.

The market’s stability, however, is juxtaposed with an undercurrent of economic volatility. The first trading week revealed “limited activity” from institutional investors, primarily due to uncertainty regarding economic conditions. This cautious approach has prompted dealers and strategists to comment on the tentative stance taken by many players in the market. According to Birch Creek’s analysts, as economic conditions display volatility, participants remain hesitant to embrace large transactions, reflecting broader apprehensions about market locality.

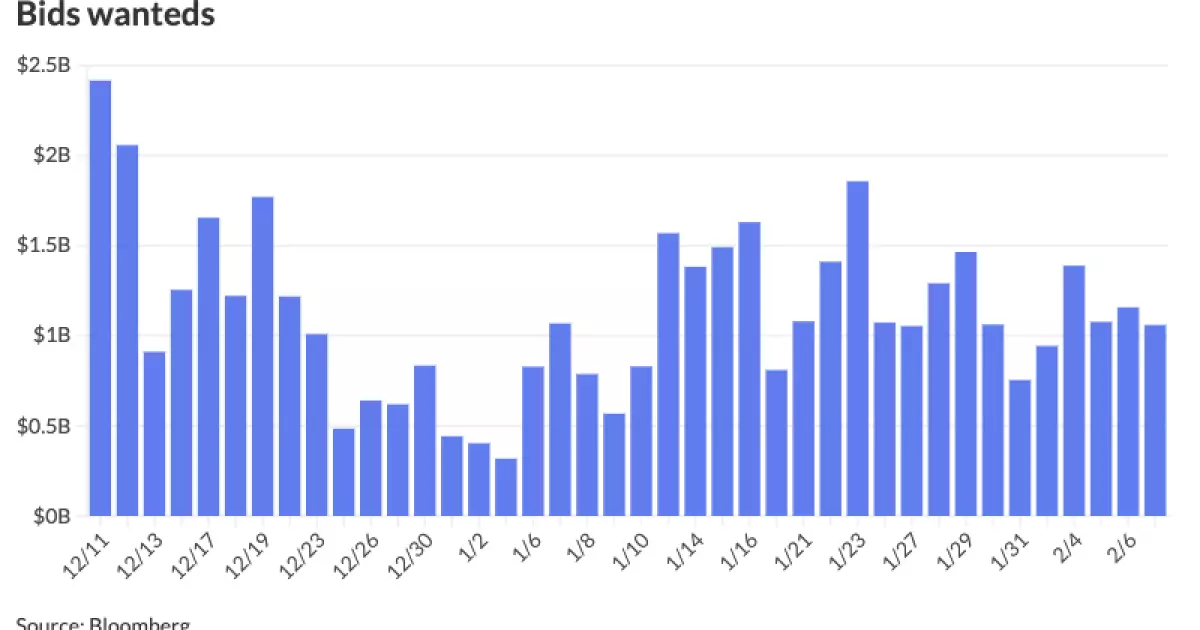

Despite initial hesitancy, as the new week progressed, factors such as substantial reinvestment cash along with an accommodating new issue calendar played pivotal roles in rekindling interest among investors. The influx of both customer purchases and sales is indicative of renewed confidence among market participants. Reports indicate dealer sales surged by 26% compared to recent averages, with demand for bid wanted shares increasing by 20%. This emerging activity level suggests a shift in investor mentality, with a growing inclination to not only engage but also capitalize on perceived opportunities.

Municipals have outperformed U.S. Treasuries (USTs), as illustrated by noteworthy adjustments in the ratio of municipal yields relative to USTs. Wong highlighted that this trend is particularly observable in the two- to ten-year range, with ratios tightening by approximately 2 percentage points since the year commenced. Conversely, the 30-year segment has experienced a relative cheapening against USTs, surpassing declines witnessed previously, with a significant rise noted since December.

The attractiveness of the municipal bond market has been further underscored by sizable flows into mutual funds and exchange-traded funds. Clements pointed out the astounding $5.2 billion accumulated in the municipal market year-to-date, with a notable 40% directed towards high-yield strategies and 62% attracted to long-duration securities. This suggests that investors are strategically positioning themselves towards sectors that promise enhanced returns amid the current yield landscape.

Indeed, this trend toward high-yield and long-duration strategies illustrates a broader institutional and retail shift. Investors appear to be mindful of the steepness of the muni curve, absorbing the implications of ongoing credit spread compression. With these dynamics at play, using municipal bonds not only as a defensive asset but also as a route to superior returns has gained appeal.

The current yield environment reveals minimal fluctuations across AAA benchmark scales. Rates, including the one-year at 2.58% and the 30-year hovering around 3.93%, exemplify a stable yield curve. However, while stability persists in top-rated municipal bonds, UST yields have exhibited a mixed trend with marginal upward and downward adjustments across different maturities.

In light of these trends, market expectations for interest rates remain an essential consideration. The yield landscape indicates investors are keenly aware of potential future movements in rates, influencing their choice to favor either short- or long-dated munis.

On the horizon, various municipalities gear up to issue substantial bonds, indicating potential shifts in demand and price pressure. Notably, the New York City Transitional Finance Authority is set to price a hefty $1.659 billion in future tax-secured bonds, while the state of Ohio follows suit with over $800 million in higher education general obligations. Each of these forthcoming issuances will inevitably affect market liquidity and pressing investor strategies as supply and demand dynamics battle for dominance.

The current landscape of the municipal bond market signals a cautious optimism. Investors are recalibrating their approaches following a setback in December, fostering a revival in activity levels and increasing confidence in long-duration and high-yield investment avenues. Moving forward, the interplay between economic indicators, interest rate expectations, and upcoming bond issuances will be pivotal in shaping the future trajectory of the municipal bond market.