As we step into 2025, the municipal bond market has started on a cautiously optimistic note, exhibiting a strengthening disposition as January reinvestment flows begin to materialize. In contrast, U.S. Treasury markets have exhibited choppy behavior, closing the session with varied performances. This article delves into the performance of municipal bonds, primary trends, and the implications for investors as they navigate the fixed-income landscape in the new year.

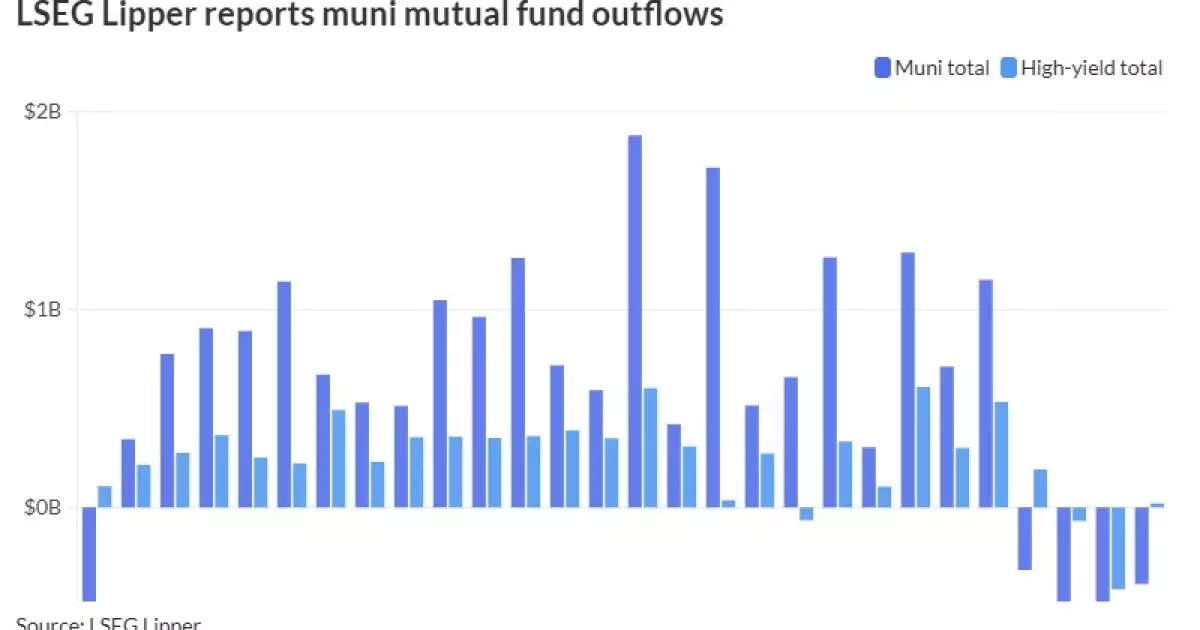

The prelude to 2025 was characterized by a notable outflow from municipal bond mutual funds. Despite an influx of January reinvestment dollars, which usually enhances market performance, the previous weeks saw investors withdraw substantial capital. For the last reporting week of 2024, municipal bond funds experienced outflows of $386.9 million, following a staggering $878.5 million in the prior week. This shift in behavior marks a critical revitalization after a solid streak of 23 weeks of inflows, indicating a potentially cautious stance as investors reassess the economic environment and returns in the fixed-income sector.

Adding a twist to this narrative, high-yield municipal bonds displayed resilience by reverting to inflows to conclude 2024 on a positive trajectory. This sector significantly outperformed, accentuating a diverging trend between high-yield and traditional investment-grade municipal bonds. The year-end yield landscape reveals a slight decline, with triple-A yields for various maturities falling by one to three basis points, contributing to a complex picture of mixed market signals.

Analyzing the overall performance metrics, municipal bonds closed 2024 with a total return of +1.05%, which was superior to the U.S. Treasury Index’s return of +0.58%, but lagged behind corporate bonds that clocked in at +2.13%. In December alone, municipal bonds suffered a total return loss of -1.46%, sparking a wave of discussions among market analysts regarding sector vulnerabilities and the broader economic implications.

Diving deeper, the Investment Grade Muni Index exhibited a multi-faceted performance across risk stratifications. Higher-risk sectors such as Investment-Grade Revenue (IDR) and BBB rated bonds experienced the most substantial performance boost when measured against return trendlines. Conversely, long-duration bonds bear the brunt of losses, not only in December but also throughout the year. The decline in the 30s10s MMD slope from 119 basis points to 84 basis points underscores the unsettling behavior of long-dated assets amid shifting investor preferences.

Looking ahead, there remains robust enthusiasm tempered with caution regarding the municipal bond market as 2025 unfolds. Market experts posit that the foundation of performance in this sector will largely hinge on stable economic conditions that safeguard revenue streams for associated projects. Should U.S. Treasury rates trend lower, the economics of advance refundings could improve significantly, thus potentially bolstering tax-exempt municipal financing and resulting in a gratifying boost to bond volumes.

Notably, taxable municipal indexes have struggled, finishing the year with -2.46%, reflecting subpar performance compared to other taxable fixed-income products. Despite this, the full-year result for taxable munis still ended with a modest 1.5% gain, slightly surpassing Treasury and Aggregate indexes. This differential showcases the nuanced nature of municipal finance, where various classifications react distinctly to common economic pressures.

The oscillation between inflows and outflows among municipal bond funds throughout 2024 points to a complex investor psyche. Despite substantial net outflows for four consecutive weeks towards the year’s end, high-yield bonds still managed noticeable inflows, correlating with their perceived resilience and stability relative to riskier asset classes. Notably, the Investment Company Institute highlighted a remarkable $1.296 billion in outflows in December alone, underscoring the challenges facing the municipal marketplace in retaining investor confidence amid rising Treasury yields.

Moreover, with a collective $2.079 billion influx into tax-exempt money market funds further amplifying existing market dynamics, the average yield here has increased to a commendable 3.19%. The attraction provided by such yields will likely continue to entice liquidity into the municipal space, impacting bond pricing and yields as the market corrects itself for 2025.

As the environment for municipal bonds continues to evolve in 2025, the interplay between stabilizing economic conditions and investor behavior will be crucial. While December’s performance serves as a reminder of inherent risks, growth in certain sectors, particularly high-yield munis, suggests that cautious optimism may prevail. Investors must remain vigilant, drawing on analytical insights to navigate this complex landscape effectively, aiming to capitalize on emerging opportunities while hedging against potential adversities. The municipal bond market’s response to broader economic trends will invariably shape its trajectory in the months to come.