In the labyrinthine corridors of the current financial landscape, the recent quiet in bond markets appears more than mere pause—it’s an ominous whisper of underlying shifts. While the headlines highlight marginal declines in munis and Treasuries, a deeper analysis reveals that these seemingly minor movements are more indicative of a brewing change than a pause. The bond markets are notoriously contrarian; what looks like stability often masks an impending reconfiguration of investor confidence. It’s easy to dismiss a few basis point adjustments as trivial, but seasoned market watchers know better. These small, incremental moves are the canaries in the coal mine, signaling a recalibration of risk appetite, valuation expectations, and supply-demand imbalances.

What’s particularly striking is the divergence between equities and fixed income. While stocks marched upward—an optimistic sign—bond yields edged higher, hinting at a possible shift in the investment narrative. The slight upticks in muni yields, coupled with broader treasury movements, suggest markets are digesting new supply pressures, inflation expectations, and central bank stances. Such a cautious standstill could be a strategic moment, allowing investors to brace for more turbulence or to reassess their positions as supply begins to swell again in the months ahead.

The Anatomy of a Potential Turnaround

The small yield increases—up to four basis points on munis—aren’t mere market noise. They reflect a complex interplay of supply management, investor behavior, and macroeconomic signals. The figures from Municipal Market Data and ICE Data Services align in painting a picture of a market that’s overextended but still resilient. The muni-to-U.S. Treasury ratios—especially the 30-year at nearly 90%—highlight how bond valuations have become almost detached from fundamental risk measures.

These ratios matter because they expose how investors view munis relative to Treasuries. Elevated ratios often suggest that munis are attractively undervalued, encouraging risk-taking but also signaling potential overheating. The small movements and the slight steepening in yield curves suggest investors are beginning to price in a tapering of the aggressive rally, perhaps anticipating a more cautious stance from policymakers, or a supply uptick in the fall. The question remains: is this a temporary correction or the beginning of a more enduring shift?

Indeed, the rally’s extension has rewarded those daring enough to buy long-term bonds—gains on the 22-year and longer indexes so far in September are impressive. Still, that outperformance could be short-lived if inflation pressures intensify or if the Federal Reserve signals tighter monetary policies. For now, the market seems to be riding a fine line, balancing between optimism and caution, with valuations stretched but still holding.

The Political and Economic Implications of Market Movements

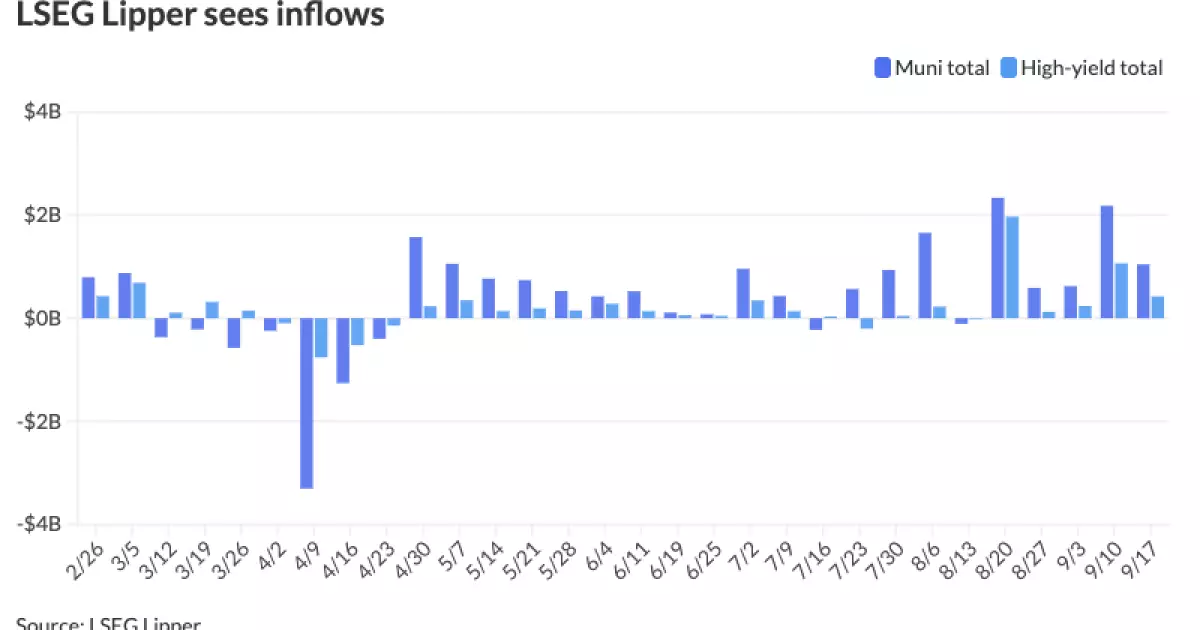

These micro-adjustments in bond yields carry significant political and economic weight, particularly within a centrist-liberal framework that values fiscal prudence combined with economic growth. The steady inflows into municipal funds—over a billion dollars last week—highlight that investors still see long-term value in municipal bonds, especially amid uncertainties. Yet, the moderation of inflows suggests a strategic pause rather than renewed enthusiasm.

From a policy standpoint, the current yields and market orders hint toward a cautious stance from both investors and policymakers. Centers of power are aware that excessive valuation gaps and inverted curves—particularly within the five-year to 2030 range—could suppress long-term growth if left unchecked. The fact that yields remain close to or above 2% for AAA rated munis signals a market reluctant to push valuations too high without regard for risk. Acknowledging the limits of fiscal stimulus and the importance of responsible debt management becomes crucial in this environment.

Moreover, the recent upticks in treasury yields reflect evolving concerns about inflation and debt sustainability. These signals prompt a nuanced approach: continued support to foster economic recovery, but with vigilance against overheating. Progressively rising yields and stable swap indices suggest a cautious optimism, but also a recognition that balance must be maintained to prevent future volatility.

The Broader Outlook: Small Adjustments as Catalysts

It’s tempting to view the current market pauses as just that—pauses. But in reality, they are strategic junctures where the next move could be anything from stabilization to a sharp correction. The subtle movements in yields, curves, and fund flows emphasize that markets are in a delicate dance, teetering between a basking in recent gains and preparing for potential headwinds.

For those aligned with a center-right liberal perspective, the key takeaway is not to dismiss these small changes as inconsequential. Instead, they serve as warnings—a reminder that financial markets, much like political realities, are susceptible to overextensions and outliers. Responsible stewardship, prudent risk management, and forward-looking policies are more vital now than ever, ensuring that brief periods of overconfidence do not spiral into systemic vulnerabilities.

Ultimately, these micro shifts are the market’s way of telling us to stay vigilant, question assumptions, and recognize that in the intricate web of investments, even the tiniest move can herald significant change.